Philip Morris Stock: Buy This 5.4% Yielding Dividend Aristocrat Now

[ad_1]

Andrey Maximenko/iStock via Getty Images

Ben Graham, one of the greatest investors in history and Buffett’s mentor, famously said

In the short-run, the market is a voting machine — reflecting a voter-registration test that requires only money, not intelligence or emotional stability — but in the long-run, the market is a weighing machine.”

25 million new investors since the pandemic might have been unaware of this timeless wisdom, as evidenced by the craziness of the last few years.

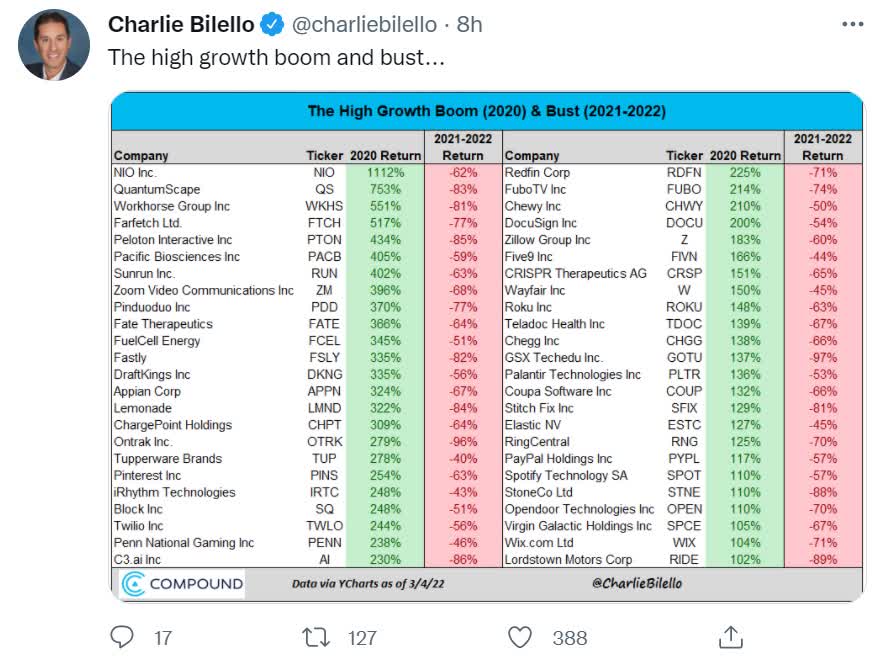

Charlie Bilello

For example, at its peak, Zoom (ZM), one of the pandemic growth darlings, was trading at 125X sales. Not earnings, sales.

For context, during the tech bubble, Sun Microsystems CEO said that 10X sales were a crazy price to pay for even the best growth stocks.

Well, as you can see, speculators in Zoom who ignored valuations are learning a painful lesson in market reality.

Rule number one: most things will prove to be cyclical.

Rule number two: some of the greatest opportunities for gain and loss come when other people forget rule number one.” – Howard Marks

And Zoom is hardly the only example of stock market madness we’ve seen in the last two years.

Charlie Bilello

Some of the hottest pandemic names are down 70%, 80%, or even 97% from their February 2021 highs.

What’s my point? That the stock market can be hilariously, and profitably wrong in the short-term.

- according to JPMorgan, in the short term, luck and momentum are 33X as powerful as fundamentals

- according to Fidelity, in the very long term, fundamentals are 33X as powerful as luck

Today, I wanted to highlight the four reasons why the market is dead wrong about Philip Morris (PM), one of the world’s highest quality high-yield dividend kings.

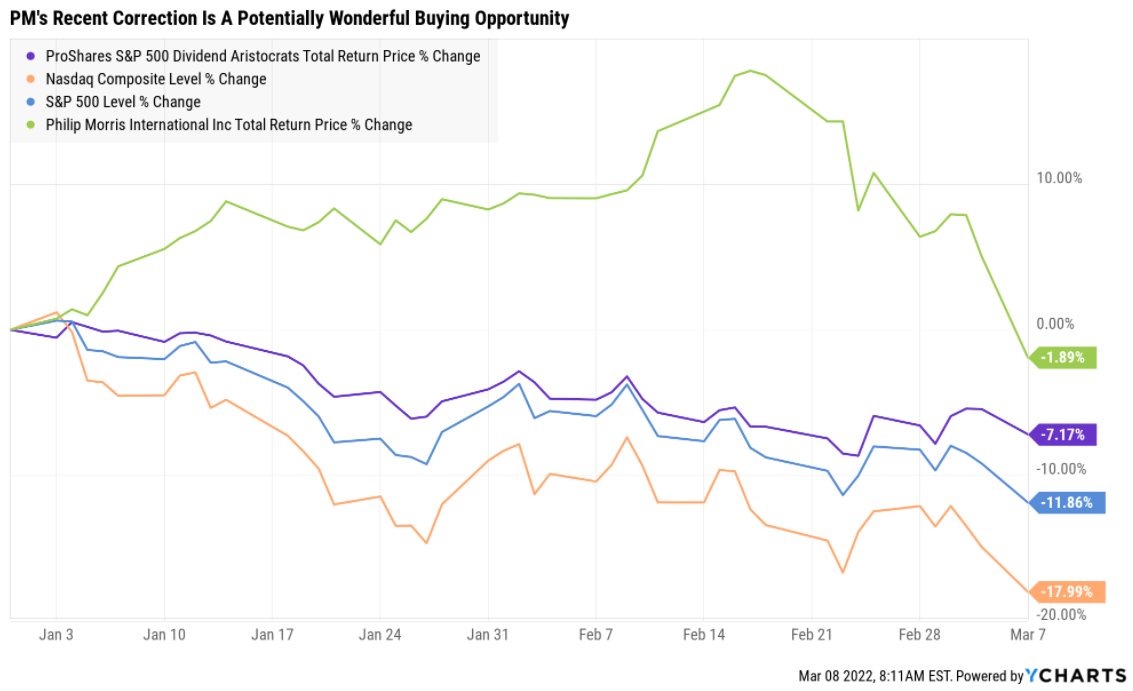

YCharts

PM is still up this year, easily outperforming the dividend aristocrats, S&P and Nasdaq. However, it recently fell 17% in a matter of days, including 6.6% on Monday, March 7th.

After a thorough and comprehensive examination of the best available facts we have today, I believe there is one simple conclusion we can draw.

Buy Philip Morris now, before everyone else does. In fact, I used PM’s 7% crash to buy more for my retirement portfolio.

While I can’t promise you this is the bottom, I can say with strong confidence that anyone buying PM today is likely to feel like a stock market genius in 5+ years, and here are four reasons why.

Reason 1: Russia Fears Are Overblown

Why did PM, which was one of the hottest stocks of 2022, suddenly cliff dive 17%, including almost 7% in a single day?

It’s likely due to concerns about Russia, which triggered a downgrade from JPMorgan.

JPMorgan dropped its rating on Philip Morris International to Neutral from Overweight due to near-term headwinds.

On the positive side, the firm noted that the tobacco giant is the global leader in both cigarettes and heated tobacco products, as well as being on track to cash in on nearly $10B of cumulative new generation products investments. On the negative side, JPMorgan analysts warned that the recent geopolitical can not be ignored.

“However, the recent tensions in Ukraine have clouded PMI’s ability to achieve its near and medium-term NGP targets, with Russia and Ukraine accounting for 23% of its HTU volume. Although the MT growth algorithm remains robust (FY21-24e organic sales/EBIT/EPS CAGR of +6%/+11%/+13%) driven by the highly attractive economics of HTP and an un-stretched balance sheet provides buyback support, external factors will prove too difficult to overcome.” – Seeking Alpha

First of all, JPMorgan is not saying the long-term thesis is intact. In fact, they expect EPS growth of 13% through 2024.

- higher than the median analyst consensus of 10.3%

JPMorgan is basically saying that they don’t think that PM is likely to outperform in the SHORT-TERM due to the temporary headwinds of the Russian invasion.

Why?

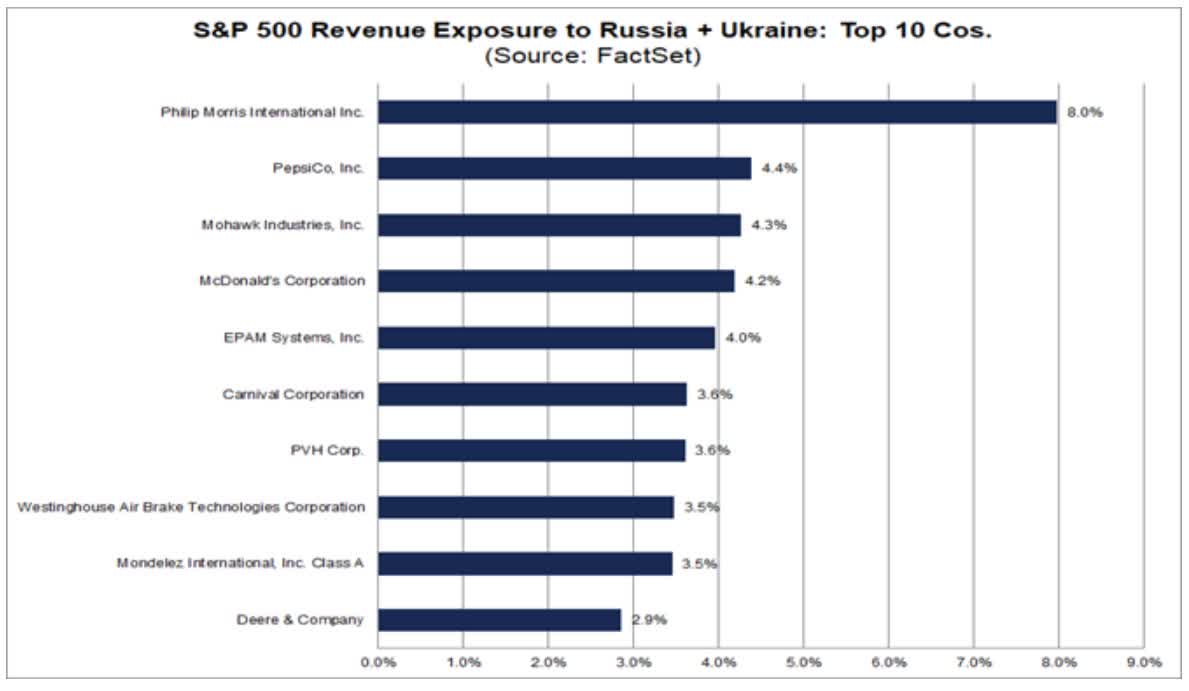

FactSet

Because no US company has more revenue from Russia and Ukraine than PM.

In fact, 23% of IQOS volumes are from these countries though overall sales are just 8% (6% Russia, 2% Ukraine).

PM temporarily suspended operations in Ukraine due to the war. Russian operations and sales continue though the collapse of the Ruble means a potential sharp decrease in sales in the coming months.

- Russia’s GDP could fall 35% in the next year according to JPMorgan

Are these serious challenges to PM? Absolutely.

Are they thesis-shattering events? Do they permanently reduce the company’s free cash flow generating capacity by 7% to 17% as the recent price decline might have you believe?

Almost certainly not and here’s the proof.

Pre-invasion, PM’s median growth consensus from all 19 analysts that covered it was 10.7% CAGR.

- management’s guidance 9+%

What do analysts expect now that they’ve had time to digest this bad news?

10.3% long-term growth. I don’t know about you but a very safe 5.4% yield and double-digit long-term growth potential sound like a mighty attractive investment proposition.

Now, let’s consider the world’s leading experts on fundamental risk, credit rating agencies, and the bond market.

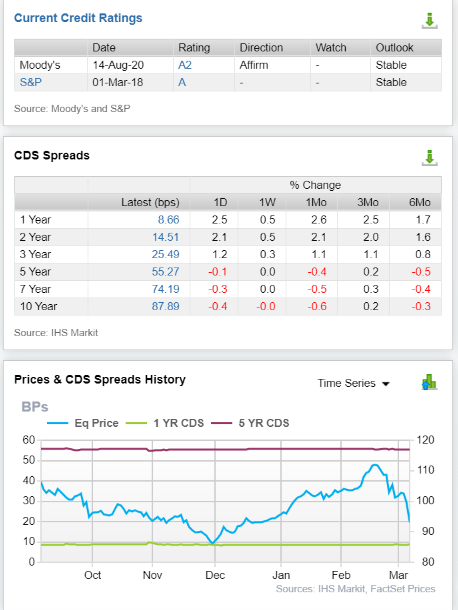

Source: FactSet Research Terminal

S&P, Fitch, and Moody’s all still rate PM A stable, indicating a 0.66% 30-year risk of default (bankruptcy).

The bond market, having had time to digest this news and JPMorgan’s negative short-term assessment, has responded with a yawn.

Credit default swaps are insurance policies bond investors take out against default.

The price of CDS is a real-time fundamental risk assessment that is always changing as news breaks and the most conservative income investors on earth update their collective estimates of a company’s bankruptcy risk.

Russia invaded on February 24th. JPMorgan downgraded PM on March 7th.

And a day later, the bond market’s estimate of PM’s fundamental risk is…

- 0.0866% chance of default in the next year, up just 2.5 basis points

- 0.88% risk of a default in the next decade, down 0.4 basis points since yesterday

In the last six months, PM’s CDS has been rock steady, during PM’s wild price swings.

What does this tell us? That after digesting the new information, analysts, rating agencies, and the bond market all agree that PM’s long-term thesis is intact.

So why did PM fall 17% in a matter of days? Was it in a bubble?

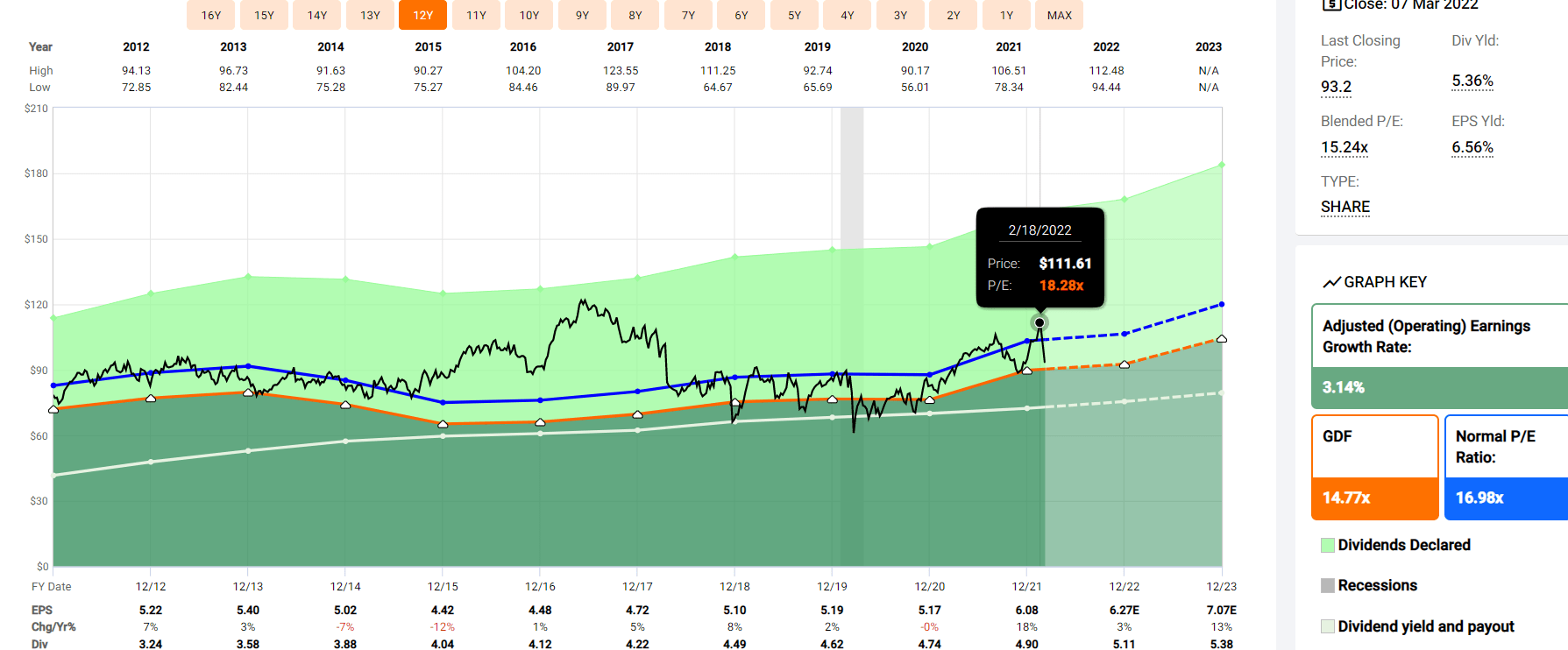

FAST Graphs, FactSet

PM was trading at 18X earnings pre-Russian invasion. It historically trades at 16.5 to 17.5.

It was not significantly overvalued and that’s why a 17% price crash in a few weeks, when the thesis is firmly intact, is such a potentially wonderful buying opportunity.

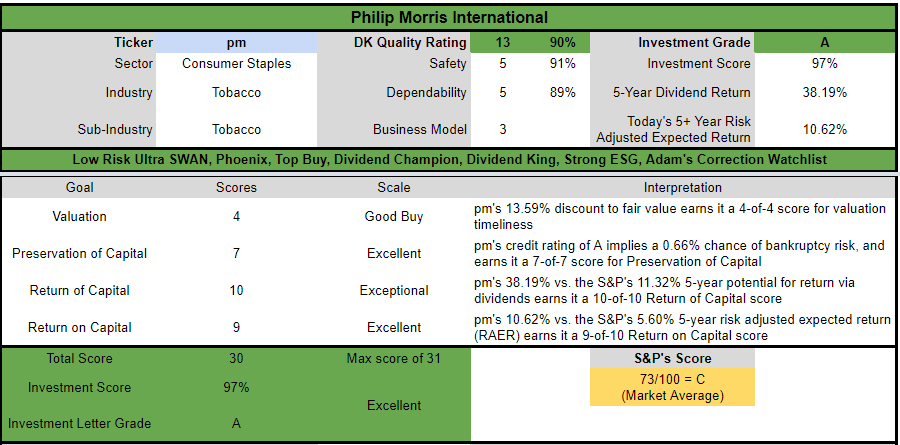

Reason 2: One Of The World’s Safest And Highest Quality Companies

The Dividend King’s overall quality scores are based on a 237 point model that includes:

-

dividend safety

-

balance sheet strength

-

credit ratings

-

credit default swap medium-term bankruptcy risk data

-

short and long-term bankruptcy risk

-

accounting and corporate fraud risk

-

profitability and business model

-

growth consensus estimates

-

historical earnings growth rates

-

historical cash flow growth rates

-

historical dividend growth rates

-

historical sales growth rates

-

cost of capital

-

long-term risk management scores from MSCI, Morningstar, FactSet, S&P, Reuters/Refinitiv, and Just Capital

-

management quality

-

dividend-friendly corporate culture/income dependability

-

long-term total returns (a Ben Graham sign of quality)

-

analyst consensus long-term return potential

It actually includes over 1,000 metrics if you count everything factored in by 12 rating agencies we use to assess fundamental risk.

How do we know that our safety and quality model works well?

During the two worst recessions in 75 years, our safety model predicted 87% of blue-chip dividend cuts during the ultimate baptism by fire for any dividend safety model.

How does PM score on one of the world’s most comprehensive safety models?

PM Dividend Safety

| Rating | Dividend Kings Safety Score (147 Point Safety Model) | Approximate Dividend Cut Risk (Average Recession) |

Approximate Dividend Cut Risk In Pandemic Level Recession |

| 1 – unsafe | 0% to 20% | over 4% | 16+% |

| 2- below average | 21% to 40% | over 2% | 8% to 16% |

| 3 – average | 41% to 60% | 2% | 4% to 8% |

| 4 – safe | 61% to 80% | 1% | 2% to 4% |

| 5- very safe | 81% to 100% | 0.5% | 1% to 2% |

| PM | 91% | 0.5% | 1.5% |

| Risk Rating | Low-Risk (77th industry percentile consensus) | A stable credit rating 0.66% 30-year bankruptcy risk | 20% OR LESS Max Risk Cap Recommendation |

Long-Term Dependability

| Company | DK Long-Term Dependability Score | Interpretation | Points |

| Non-Dependable Companies | 21% or below | Poor Dependability | 1 |

| Low Dependability Companies | 22% to 60% | Below-Average Dependability | 2 |

| S&P 500/Industry Average | 61% (58% to 70% range) | Average Dependability | 3 |

| Above-Average | 71% to 80% | Very Dependable | 4 |

| Very Good | 81% or higher | Exceptional Dependability | 5 |

| PM | 89% | Exceptional Dependability | 5 |

Overall Quality

| PM | Final Score | Rating |

| Safety | 91% | 5/5 very safe |

| Business Model | 90% | 3/3 wide moat |

| Dependability | 89% | 5/5 exceptional |

| Total | 90% | 13/13 Ultra SWAN dividend king |

| Risk Rating | 3/3 low Risk | |

| 20% OR LESS Max Risk Cap Rec |

5% Margin of Safety For A Potentially Good Buy |

PM: The 43rd Highest Quality Master List Company (Out of 509) = 92nd Percentile

The DK 500 Master List includes the world’s highest quality companies including:

-

All dividend champions

-

All dividend aristocrats

-

All dividend kings

-

All 13/13 Ultra Swans (as close to perfect quality as exists on Wall Street)

- 47 of the world’s best growth stocks (on its way to 50)

PM’s 90% quality score means it’s similar in quality to such blue-chips as

- Emerson Electric (EMR) – dividend king

- PPG Industries (PPG) – dividend aristocrat

- V.F. Corporation (VFC) – dividend king

- Procter & Gamble (PG) – dividend king

- Johnson & Johnson (JNJ) -dividend king

- BlackRock (BLK)

- Merck (MRK)

- Alphabet (GOOG)

- 3M (MMM) – dividend king

- Lowe’s (LOW) – dividend king

- Amazon (AMZN)

Even among the most elite companies on earth, PM higher quality than 92% of them.

Why is that?

PM is the industry leader in the smoke-free future transition with almost 30% of sales now coming from reduced-risk products or RRPs.

PM has the 2nd most geographic diversification behind BTI, with 39% of sales from the EU, 15% from Japan, 14% from the rest of Asia, and 32% from the rest of the world.

Iluma is the new IQOS tech that gets around BTI’s patents.

During the year, we laid the foundations for our long-term growth ambitions beyond nicotine in Wellness and Healthcare, including the milestone acquisitions of Fertin and Vectura, which provide essential capabilities for future product development.” – CEO Q4 conference call

PM was able to close on its acquisitions of medical vaporizer companies, its first steps in an effort to diversify beyond nicotine.

- $800 million in gross savings in 2021

- 10 countries with 50+% sales from RRPs

2021’s results were very strong.

- 8% sales growth

- 2% increase in operating margin

- EPS growth 15% in constant currency (18% nominal growth)

2022 guidance includes:

- 20% IQOS volume growth

- 5% sales growth

- 1% operating margin growth

- 9.5% EPS growth

Management may reduce guidance in the next earnings call, but one bad year doesn’t mean a strong investment thesis break.

- an industry volume decline of 1.5%

- PM volume decline: 0%

- $10 billion in free cash flow (78% FCF payout ratio)

PM’s 2022 guidance was so strong that 2022 is likely still to be a solid year of growth.

- analysts still expect 3% EPS growth in 2022, including the effects of a strong dollar

- the same forecast as pre-invasion

PM’s IQOS volumes were up 25% in 2021 and 17% in Q4.

IQOS was 14% of volumes in Q4, driving 31% of sales.

IQOS is the world’s 3rd most popular nicotine brand.

- Marlboro: 13% (owned by PM)

- Winston (owned by BTI)

- IQOS 7%

- L&M 4% (owned by PM)

- PM’s overall global market share: 28%

PM is on track to become a majority non-tobacco company by 2025.

In early IQOS markets, it has already reached and surpassed that goal.

- Italy 53%

- Czechia 55%

- Greece 65%

- Japan 71%

- EU 33%

- Eastern Europe 37%

- Asia 59%

In IQOS’s top 10 markets, cigarette volume declines have been about 3X faster than globally.

- PM is part of the solution to ending smoking

72% of PM smokers who try IQOS stick with it and give up smoking for good.

- no smoking cessation program in history comes close to such success rates

IQOS is currently in 71 countries and PM has plans to expand that to 100 by 2025.

- with approximately 100 more to go after that

PM is on track to achieve its goal of $1+ billion in sales of medical products by 2025.

- $450 to $600 million investments planned through 2024

PM estimates it is now targeting an $89 billion annual wellness market (in 2025) that’s growing at 11% annually.

Globally, nicotine is a $470 billion industry (up from $450 billion in 2020), growing at 4%.

- -1% volume growth (due to cigarette declines)

- 4% CAGR sales growth

- vaping: 10% to 15% CAGR growth

- heat sticks: 25+% CAGR growth

- nicotine pouches: 30% to 40% CAGR growth

PM is continuing to roll out new RRP products to keep its momentum and first-mover advantage.

Management remains confident it is on track to achieve 5+% sales growth and 9%+ earnings growth in the coming years.

And let’s not forget about PM’s industry-leading fortress balance sheet.

PM Credit Ratings

| Rating Agency | Credit Rating | 30-Year Default/Bankruptcy Risk | Chance of Losing 100% Of Your Investment 1 In |

| S&P | A stable outlook | 0.66% | 151.5 |

| Fitch | A stable outlook | 0.66% | 151.5 |

| Moody’s | A2 (A Equivalent) stable | 0.66% | 151.5 |

| Consensus | A stable outlook | 0.66% | 151.5 |

(Source: S&P, Fitch, Moody’s)

PM has the strongest credit rating of big tobacco, with a 0.66% fundamental risk.

PM Leverage Consensus Forecast

| Year | Debt/EBITDA | Net Debt/EBITDA (3.0 Or Less Safe According To Credit Rating Agencies) |

Interest Coverage (8+ Safe) |

| 2021 | 2.49 | 1.89 | 18.93 |

| 2022 | 2.29 | 1.61 | 21.48 |

| 2023 | 2.12 | 1.64 | 23.57 |

| 2024 | 2.00 | 1.50 | 25.62 |

| 2025 | 1.93 | 1.26 | 33.08 |

| Annualized Change | -6.20% | -9.54% | 14.97% |

(Source: FactSet Research Terminal)

PM’s leverage is very low and falling lower by the year.

PM Balance Sheet Consensus Forecast

| Year | Total Debt (Millions) | Cash | Net Debt (Millions) | Interest Cost (Millions) | EBITDA (Millions) | Operating Income (Millions) | Average Interest Rate |

| 2020 | $31,536 | $7,280 | $23,851 | $618 | $12,651 | $11,698 | 1.96% |

| 2021 | $33,105 | $7,280 | $23,310 | $628 | $14,478 | $13,488 | 1.90% |

| 2022 | $31,594 | $6,124 | $24,356 | $590 | $14,885 | $13,905 | 1.87% |

| 2023 | $32,129 | $6,218 | $24,193 | $593 | $16,093 | $15,193 | 1.85% |

| 2024 | $34,357 | $4,491 | $22,482 | $503 | $17,806 | $16,637 | 1.46% |

| 2025 | $35,513 | $4,491 | NA | NA | NA | $17,376 | 0.00% |

| Annualized Growth | 2.40% | -9.21% | -1.47% | -5.02% | 8.92% | 8.23% | -7.03% |

(Source: FactSet Research Terminal)

- cash stockpiled during the pandemic

- expected to come down to just under $5 billion over time

- debt rising slowly

- cash flows growing much faster

- borrowing costs are expected to fall steadily despite rising global interest rates

PM Bond Profile

- $10.8 billion in liquidity

- well staggered debt maturities (little problem refinancing maturing bonds)

- 100% unsecured bonds (maximum financial flexibility)

- bond investors so confident in PM’s long-term prospects, they are willing to lend to it for 23 years at 4.24%

- the average borrowing cost is 3.58%

- 1.4% after inflation vs 56% cash returns on invested capital

PM Profitability: Wall Street’s Favorite Quality Proxy

PM’s profitability is historically in the top 10% of peers.

PM 12-Month Profitability Vs Peers

| Metric | Industry Percentile | Major Tobacco Companies More Profitable Than PM (Out Of 48) |

| Operating Margin | 89.13 | 5 |

| Net Margin | 89.13 | 5 |

| Return On Equity | 83.33 | 8 |

| Return On Assets | NA | NA |

| Return On Capital | 83.33 | 8 |

| Average | 86.23 | 7 |

(Source: Gurufocus Premium)

Since the launch of IQOS, PM’s profitability has been rising steadily, confirming a wide and stable moat.

- free cash flow margins of 36% are in the top 5% of all companies on earth

PM Profit Margin Consensus

| Year | FCF Margin | EBITDA Margin | EBIT (Operating) Margin | Net Margin | Return On Capital Expansion |

Return On Capital Forecast |

| 2020 | 30.8% | 44.1% | 40.8% | 28.1% | 1.11 | |

| 2021 | 31.8% | 46.1% | 42.9% | 29.6% | TTM ROC | 211.55% |

| 2022 | 32.8% | 46.1% | 43.1% | 30.3% | Latest ROC | 197.76% |

| 2023 | 31.9% | 46.9% | 44.2% | 31.3% | 2025 ROC | 234.48% |

| 2024 | NA | 48.7% | 45.5% | 32.4% | 2025 ROC | 219.19% |

| 2025 | NA | NA | 47.6% | 33.5% | Average | 226.83% |

| 2026 | NA | NA | NA | NA | Industry Median | 67.14% |

| Annualized Growth | 1.22% | 2.50% | 3.15% | 3.57% | PM/Peers | 3.38 |

| Vs S&P | 15.54 |

(Source: FactSet Research Terminal)

PM’s industry-leading profitability is expected to slowly but steadily improve over time.

Return on capital is expected to modestly rise over time.

- pre-tax profit/the money it takes to run the business (operating capital)

- Joel Greenblatt’s gold standard proxy for quality and moatiness

According to one of the greatest investors in history, PM is about 16X higher quality than the average S&P 500 company.

PM’s ROC has been trending higher for 17 years.

- doubling approximately every 11 years

PM Dividend Growth Consensus

| Year | Dividend Consensus | EPS/Share Consensus | Payout Ratio | Retained (Post-Dividend) Cash Flow | Buyback Potential | Debt Repayment Potential |

| 2021 | $4.90 | $6.08 | 80.6% | $1,829 | 1.12% | 5.5% |

| 2022 | $5.15 | $6.31 | 81.6% | $1,798 | 1.10% | 5.4% |

| 2023 | $5.49 | $7.04 | 78.0% | $2,403 | 1.47% | 7.6% |

| 2024 | $5.84 | $7.89 | 74.0% | $3,178 | 1.95% | 9.9% |

| Total 2021 Through 2024 | $21.38 | $27.32 | 78.3% | $9,207.00 | 5.64% | 27.81% |

| Annualized Rate | 6.02% | 9.07% | -2.80% | 20.21% | 20.21% | 21.42% |

(Source: FactSet Research Terminal)

Rating agencies want to see 85% or less payout ratios.

- MO’s policy is 80%

- PM’s policy is 75%

- BTI’s policy is 65%

PM’s payout ratio is expected to keep falling steadily despite the fastest dividend growth in its industry.

$9.2 billion in post-dividend retained earnings is enough to pay off 28% of current debt or buy back about 6% of shares at current valuations.

| Year | Consensus Buybacks ($ Millions) | % Of Shares (At Current Valuations) | Market Cap |

| 2021 | $594.0 | 0.4% | $163,104 |

| 2022 | $3,000.0 | 1.8% | $163,104 |

| 2023 | $4,000.0 | 2.5% | $163,104 |

| 2024 | $6,000.0 | 3.7% | $163,104 |

| 2025 | $6,000.0 | 3.7% | $163,104 |

| Total 2021 Through 2025 | $19,594.00 | 12.0% | $163,104 |

| Annualized Rate | 2.52% | Average Annual Buybacks | $3,918.80 |

(Source: FactSet Research Terminal)

Analysts expect PM to rapidly accelerate buybacks in the coming years, totaling $20 billion through 2025.

PM’s future buybacks match its historical norm, which includes a long pause while it was investing $9 billion into IQOS. Since it started buying back shares in 2009, it has reduced its share count by almost 27%.

The bottom line is that PM is not a company at risk of being disrupted, it’s the leading disruptor of its industry.

And the one with the best long-term growth outlook in the industry.

Reason 3: A Strong Growth Runway For Many Years To Come

We’ve already seen how PM has turned a $9 billion investment in IQOS into the world’s 3rd most popular nicotine brand.

What does that mean for PM’s growth outlook? Well, in the long term, analysts expect 10.3% growth, in-line with management guidance.

PM Medium-Term Growth Consensus

| Year | Sales | FCF | EBITDA | EBIT (Operating Income) | Net Income |

| 2020 | $28,694 | $8,827 | $12,651 | $11,698 | $8,055 |

| 2021 | $31,405 | $9,997 | $14,478 | $13,488 | $9,292 |

| 2022 | $32,280 | $10,586 | $14,885 | $13,905 | $9,779 |

| 2023 | $34,350 | $10,957 | $16,093 | $15,193 | $10,752 |

| 2024 | $36,586 | NA | $17,806 | $16,637 | $11,863 |

| 2025 | $36,502 | NA | NA | $17,376 | $12,211 |

| Annualized Growth | 4.93% | 7.47% | 8.92% | 8.23% | 8.68% |

(Source: FactSet Research Terminal)

Management says it can drive 5% top line growth and that’s what analysts expect.

| Metric | 2020 Growth | 2021 Growth Consensus | 2022 Growth Consensus | 2023 Growth Consensus | 2024 Growth Consensus |

2025 Growth Consensus |

| Sales | -4% | 9% | 3% | 7% | 6% | 0% |

| Dividend | 3% | 3% | 4% (Official) | 7% | 6% | NA |

| EPS | 0% | 18% | 3% | 13% | 10% | 2% |

| Operating Cash Flow | -2% | 22% | -6% | 7% | 16% | NA |

| Free Cash Flow | 8% | 13% | 3% | 7% | NA | NA |

| EBITDA | 1% | 7% | 6% | 10% | 9% | NA |

| EBIT (operating income) | 1% | 7% | 6% | 11% | 8% | NA |

(Source: FAST Graphs, FactSet Research)

PM’s dividend growth is expected to accelerate now that its payout ratio has fallen to management’s target levels.

| Investment Strategy | Yield | LT Consensus Growth | LT Consensus Total Return Potential | Long-Term Risk-Adjusted Expected Return |

Long-Term Inflation And Risk-Adjusted Expected Returns |

| Philip Morris | 5.4% | 10.3% | 15.7% | 11.0% | 8.8% |

| Dividend Growth | 1.6% | 12.6% | 14.2% | 9.9% | 7.8% |

| Value | 2.1% | 12.1% | 14.1% | 9.9% | 7.7% |

| High-Yield | 2.8% | 11.3% | 14.1% | 9.9% | 7.7% |

| High-Yield + Growth | 1.7% | 11.0% | 12.7% | 8.9% | 6.7% |

| Safe Midstream | 5.8% | 6.3% | 12.1% | 8.5% | 6.3% |

| Safe Midstream + Growth | 3.3% | 8.5% | 11.8% | 8.3% | 6.1% |

| Nasdaq (Growth) | 0.8% | 10.7% | 11.5% | 8.1% | 5.9% |

| Dividend Aristocrats | 2.2% | 8.9% | 11.1% | 7.8% | 5.6% |

| REITs + Growth | 1.8% | 8.9% | 10.6% | 7.4% | 5.2% |

| S&P 500 | 1.4% | 8.5% | 9.9% | 6.9% | 4.8% |

| REITs | 3.0% | 6.5% | 9.5% | 6.6% | 4.4% |

| 60/40 Retirement Portfolio | 1.9% | 5.1% | 7.0% | 4.9% | 2.7% |

| 10-Year US Treasury | 1.7% | 0.0% | 1.7% | 1.2% | -1.0% |

(Source: Morningstar, FactSet, YCharts)

Analysts expect PM to potentially deliver almost 16% long-term returns, far more than the aristocrats, S&P, or Nasdaq.

In fact, it’s more than just about any major investment strategy on Wall Street.

- Private equity strives for 15% returns and requires 7 to 15 years of lockups on your money

- PM offers instant liquidity, a very safe 5.4% yield, and long-term return potential on par with the greatest investors in history

Inflation-Adjusted Long-Term Consensus Return Potential: $1,000 Initial Investment

| Time Frame (Years) | 7.8% CAGR Inflation-Adjusted S&P Consensus | 8.9% Inflation-Adjusted Aristocrat Consensus | 13.5% CAGR PM Consensus | Difference Between Fast-Growing Aristocrat Consensus And S&P |

| 5 | $1,453.07 | $1,531.58 | $1,883.56 | $430.48 |

| 10 | $2,111.43 | $2,345.73 | $3,547.80 | $1,436.37 |

| 15 | $3,068.06 | $3,592.68 | $6,682.48 | $3,614.42 |

| 20 | $4,458.12 | $5,502.47 | $12,586.86 | $8,128.74 |

| 25 | $6,477.98 | $8,427.47 | $23,708.09 | $17,230.11 |

| 30 | $9,412.99 | $12,907.33 | $44,655.59 | $35,242.60 |

(Source: DK Research Terminal, FactSet)

While analysts expect the S&P to deliver 9X real return in the next 30 years, PM’s superior growth and yield could potentially deliver 45X returns.

That’s enough to turn a modest investment today into a small fortune in the coming decades.

| Time Frame (Years) | Ratio Aristocrats/S&P | Ratio PM Consensus and S&P |

| 5 | 1.05 | 1.30 |

| 10 | 1.11 | 1.68 |

| 15 | 1.17 | 2.18 |

| 20 | 1.23 | 2.82 |

| 25 | 1.30 | 3.66 |

| 30 | 1.37 | 4.74 |

(Source: DK Research Terminal, FactSet)

And that means potentially 5X better inflation-adjusted returns than the S&P 500 while you enjoy almost 4X better and safer yield.

Reason 4: A Wonderful Company At A Wonderful Price

PM started its current correction basically at fair value. And here’s what a 17% overreaction by Mr. Market means for investors today.

| Metric | Historical Fair Value Multiples (13-Years) | 2021 | 2022 | 2023 | 2024 | 2025 |

12-Month Forward Fair Value |

| 5-Year Average Yield | 5.35% | $91.59 | NA | NA | $109.16 | NA | |

| 13-year median Yield | 4.47% | $109.62 | NA | NA | $130.65 | NA | |

| 14-year average yield | 4.68% | $104.70 | $106.84 | $106.84 | $124.79 | NA | |

| Earnings | 16.98 | $103.24 | $107.14 | $119.54 | $133.97 | $136.35 | |

| Average | $101.84 | $106.99 | $112.83 | $123.87 | $136.35 | $108.00 | |

| Current Price | $93.20 | ||||||

|

Discount To Fair Value |

8.48% | 12.89% | 17.40% | 24.76% | 31.65% | 13.70% | |

|

Upside To Fair Value (NOT Including Dividends) |

9.27% | 14.80% | 21.06% | 32.90% | 46.30% | 15.88% (21% including dividend) | |

| 2022 EPS | 2023 EPS | 2021 Weighted EPS | 2022 Weighted EPS | 12-Month Forward EPS | 12-Month Average Fair Value Forward PE |

Current Forward PE |

|

| $6.29 | $7.02 | $5.20 | $1.22 | $6.42 | 16.8 | 14.5 |

(Source: DK Research Terminal, FactSet)

PM is historically worth about 17X earnings and today trades at 14.5X forward earnings.

It’s about 14% undervalued and if it returns to fair value and grows as expected in the next year, that’s about a 21% total return.

|

Analyst Median 12-Month Price Target |

Morningstar Fair Value Estimate |

| $113.89 (17.8 PE) | $108.00 (16.8 PE) |

|

Discount To Price Target (Not A Fair Value Estimate) |

Discount To Fair Value |

| 18.17% | 13.70% |

|

Upside To Price Target (Not Including Dividend) |

Upside To Fair Value (Not Including Dividend) |

| 22.20% | 15.88% |

|

12-Month Median Total Return Price (Including Dividend) |

Fair Value + 12-Month Dividend |

| $118.89 | $113.00 |

|

Discount To Total Price Target (Not A Fair Value Estimate) |

Discount To Fair Value + 12-Month Dividend |

| 21.61% | 17.52% |

|

Upside To Price Target ( Including Dividend) |

Upside To Fair Value + Dividend |

| 27.56% | 21.24% |

Morningstar’s fair value estimates match mine exactly.

And analysts expect PM to deliver 28% total returns in the next 12 months, a forecast that’s nearly all justified by its strong fundamentals.

| Rating | Margin Of Safety For Low-Risk 13/13 Ultra SWAN Quality Companies | 2022 Price | 2023 Price |

12-Month Forward Fair Value |

| Potentially Reasonable Buy | 0% | $106.99 | $112.83 | $108.00 |

| Potentially Good Buy | 5% | $101.64 | $107.19 | $102.60 |

| Potentially Strong Buy | 15% | $90.94 | $95.91 | $91.80 |

| Potentially Very Strong Buy | 25% | $76.23 | $84.62 | $81.00 |

| Potentially Ultra-Value Buy | 35% | $69.54 | $73.34 | $70.20 |

| Currently | $93.20 | 12.89% | 17.40% | 13.70% |

|

Upside To Fair Value (Not Including Dividends) |

14.80% | 21.06% | 15.88% |

For anyone comfortable with the risk profile, PM is a potentially good buy, bordering on a strong buy, and here’s why.

PM Consensus Return Potential

For context, the S&P 500 is still overvalued, but a lot less than at the start of the year.

| Year | EPS Consensus | YOY Growth | Forward PE | Blended PE | Overvaluation (Forward PE) |

Overvaluation (Blended PE) |

| 2021 | $206.39 | 50.44% | 20.4 | 23.1 | 18% | 31% |

| 2022 | $223.03 | 8.06% | 18.8 | 19.6 | 9% | 11% |

| 2023 | $245.83 | 10.22% | 17.1 | 18.0 | -1% | 2% |

| 2024 | $272.94 | 11.03% | 15.4 | 16.2 | -10% | -8% |

| 12-Month forward EPS | 12-Month Forward PE | Historical Overvaluation | PEG | 25-Year Average PEG | S&P 500 Dividend Yield |

25-Year Average Dividend Yield |

| $225.60 | 18.622 | 10.65% | 2.19 | 3.62 | 1.43% | 2.01% |

(Source: DK S&P 500 Valuation & Total Return Tool)

At the moment, the S&P 500 is a 9% further decline away from historical fair value, a forward PE of 16.8 (25-year average).

S&P 500 2023 Consensus Return Potential

FAST Graphs, FactSet

The S&P 500 is now at a valuation that offers basically flat total returns for the next two years.

S&P 500 Consensus Total Return Profile

| Year | Upside Potential By End of That Year | Consensus CAGR Return Potential By End of That Year | Probability-Weighted Return (Annualized) |

Inflation And Risk-Adjusted Expected Returns |

| 2027 | 43.34% | 7.47% | 5.60% | 2.37% |

(Source: Dividend Kings S&P 500 Valuation And Total Return Potential Tool)

Over the next five years, analysts expect a respectable 7.5% annual return from the S&P, which is about 5.5% on a risk-adjusted basis.

However, the bond market expects 3.3% inflation to turn that into a far more modest 2.4% real return.

- S&P 500’s historical inflation-adjusted return is 6% to 7%

- the bond market thinks the S&P needs to deliver 8.2% to 9.2% CAGR to deliver its historical inflation-adjusted returns in the future

And here’s what the power of high-yield Ultra SWAN value investing.

PM 2023 Consensus Total Return Potential

FAST Graphs, FactSet

If PM grows as expected and returns to fair value, it could deliver 20% annual returns through 2023.

- Buffett-like returns from a blue-chip bargain hiding in plain sight

FAST Graphs, FactSet

If PM grows as expected through 2027 and returns to fair value, that’s 117% total returns, or 14% annually. That’s about 3X more than the S&P 500 consensus.

PM Investment Decision Score

DK DK Automated Investment Decision Tool

For anyone comfortable with its risk profile, PM is one of the most reasonable and prudent high-yield blue chips you can buy today.

Risk Profile: Why Philip Morris Isn’t Right For Everyone

There are no risk-free companies and no company is right for everyone. You have to be comfortable with the fundamental risk profile.

PM’s Risk Profile Summary

- regulatory risk (plain packaging, menthol bans, nicotine level regulation, RRP tax policy)

- failure of the smoke-free transition plan: every tobacco company is trying the same strategy, BTI’s RRPs are gaining market share

- margin compression risk: RRPs are more profitable than cigarettes but only due to preferential tax treatment

- litigation risk: BTI and PM are suing each other over RRP patents around the world (PM recently won a case in Germany)

- supply chain disruption risk (strong negative effects in 2021)

- legal liability risk (though not as high as it was in the Master Settlement period)

- M&A execution risk (PM tried to buy MO back in 2018)

- labor retention risk (tightest job market in over 50 years and finance is a high paying industry)

- currency risk (significant since all sales are outside the US)

How do we quantify, monitor, and track such a complex risk profile? By doing what big institutions do.

Material Financial ESG Risk Analysis: How Large Institutions Measure Total Risk

Here is a special report that outlines the most important aspects of understanding long-term ESG financial risks for your investments.

- ESG is NOT “political or personal ethics based investing”

- it’s total long-term risk management analysis

ESG is just normal risk by another name.” Simon MacMahon, head of ESG and corporate governance research, Sustainalytics” – Morningstar

ESG factors are taken into consideration, alongside all other credit factors, when we consider they are relevant to and have or may have a material influence on creditworthiness.” – S&P

ESG is a measure of risk, not of ethics, political correctness, or personal opinion.

S&P, Fitch, Moody’s, DBRS (Canadian rating agency), AM Best (insurance rating agency), R&I Credit Rating (Japanese rating agency), and the Japan Credit Rating Agency have been using ESG models in their credit ratings for decades.

- credit and risk management ratings make up 41% of the DK safety and quality model

- dividend/balance sheet/risk ratings make up 82% of the DK safety and quality model

Dividend Aristocrats: 67th Industry Percentile On Risk Management (Above-Average, Medium Risk)

PM Long-Term Risk Management Consensus

| Rating Agency | Industry Percentile |

Rating Agency Classification |

| MSCI 37 Metric Model | 57.0% | BBB Average |

| Morningstar/Sustainalytics 20 Metric Model | 92.2% |

22.9/100 Medium-Risk |

| Reuters’/Refinitiv 500+ Metric Model | 98.4% | Excellent |

| S&P 1,000+ Metric Model | 60.0% |

Above (Positive Trend) |

| Consensus | 76.9% | Good |

| FactSet Qualitative Assessment | Above-Average | Positive Trend |

(Sources: MSCI, Morningstar, Reuters’, S&P, FactSet Research)

PM’s Long-Term Risk Management Is The 103rd Best In The Master List (79th Percentile)

PM’s risk-management consensus is in the top 21% of the world’s highest quality companies and similar to that of such other companies as

- Visa (V)

- NextEra Energy Partners (NEP)

- Bank of Montreal (BMO)

- Air Products and Chemicals (APD) – dividend aristocrat

- Verizon (VZ)

- Bristol-Myers (BMY)

- Canadian Imperial Bank of Commerce (CM)

- Enterprise Products Partners (uses K-1 tax form) (EPD)

- Diageo (DEO)

- Toronto-Dominion Bank (TD)

- V.F. Corp – dividend king

The bottom line is that all companies have risks, but PM is good at managing theirs.

How We Monitor PM’s Risk Profile

- 19 analysts

- 3 credit rating agencies

- 7 total risk rating agencies

- 26 experts who collectively know this business better than anyone other than management

- and the bond market for real-time fundamental risk analysis

When the facts change, I change my mind. What do you do sir?” – John Maynard Keynes

There are no sacred cows at iREIT or Dividend Kings. Wherever the fundamentals lead, we always follow. That’s the essence of disciplined financial science, the math retiring rich and staying rich in retirement.

Bottom Line: The Market Is Dead Wrong About Philip Morris So Buy It Now Before Everyone Else Does

I know it can feel frustrating when a blue-chip’s positive momentum is broken, especially for tobacco giants who have suffered through a multi-year bear market.

However, the reason that long-term value investing works at all is very simple. The market’s definition of “long-term” is far longer than most people realize.

This is why wonderful companies with steadily growing sales, earnings, cash flows, and dividends can spend YEARS in bear markets that aren’t justified by fundamentals.

And it’s also why low-quality companies with questionable fundamentals can stay red hot for so long.

This is why it’s important to remember that Ben Graham’s weighing machine is always active and operating, even if it’s behind the scenes during bear markets and bubbles.

Today, PM is once again suffering, at least in the short term. That’s thanks to concerns about Russian and Ukrainian sales.

But when we analyze the company fully, meaning its balance sheet safety, growth runway, brands, management, dividend dependability, and long-term risk management prowess, one thing becomes clear.

PM is one of the highest safest, most dependable, and highest quality 5% yielding dividend aristocrats on Wall Street.

Today, it is 13% undervalued, and thanks to its generous 5.4% yield and industry-leading 10% growth prospects, represent one of the smartest choices for a diversified and prudently risk-managed portfolio.

That’s why I just bought more PM and you might want to do the same.

[ad_2]

Source link